Engagement & Retention project | Simpl

Figure out the retention data for your product. If you don't have access to the same, begin by adjusting the industry standards. Plot down the data and bring to life your retention curve. Draw out observations and insights from the same.

What is causing your users to churn?

Go back to your user insights and figure out the number one reason of churn by listing down all the factors.

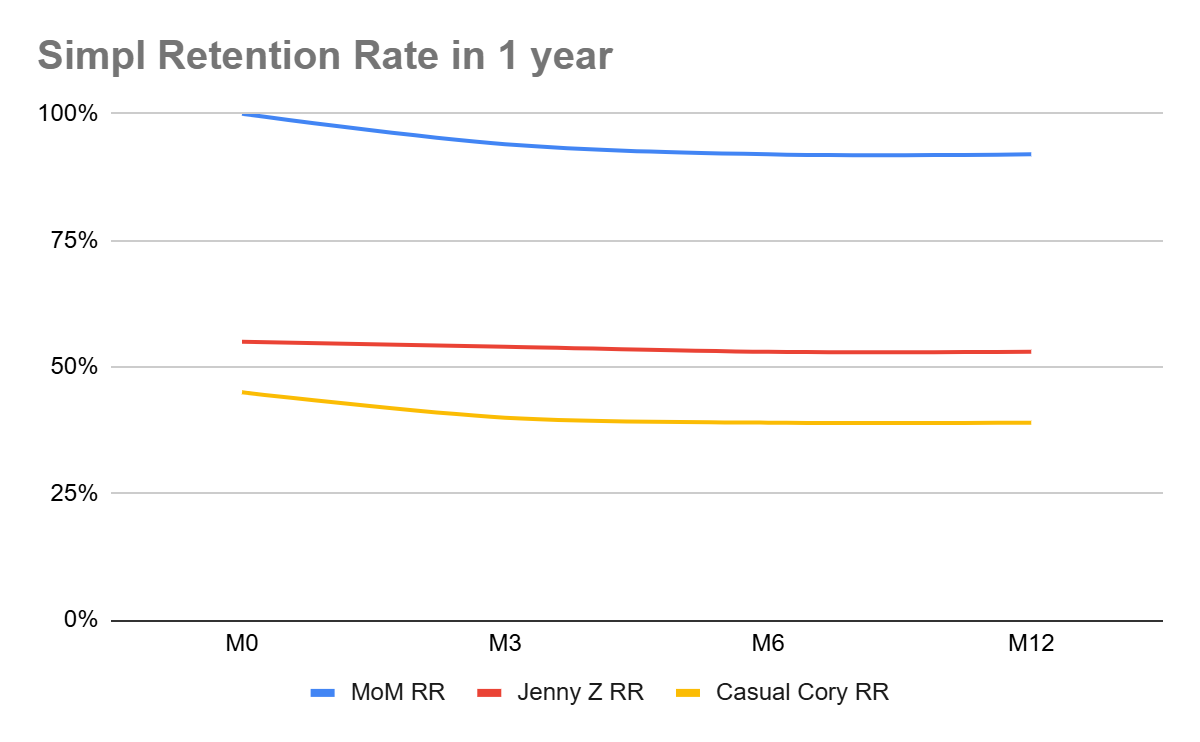

Simpl's retention rate is 90% - 95% as obtained through secondary data :

The current user base for Simpl is 25 Million

MoM RR | Total Users | Jenny Z RR | Jenny Z Users | Casual Cory RR | Casual Cory Users | |

M0 | 100% | 25 | 55% | 13.75 | 45% | 11.25 |

M3 | 94% | 23.5 | 54% | 7.425 | 40% | 4.5 |

M6 | 92% | 23 | 53% | 7.2875 | 39% | 4.3875 |

M12 | 92% | 23 | 53% | 7.2875 | 39% | 4.3875 |

Insights & Observations

Both ICPs have a smilar retention rate, however the number of Jenny Z users is higher that Casual Cory. The reason for that is word of mouth is very strong in Jenny Z. This ICP is advocating for Simpl. The reason why the retention curve for Jenny Z is slightly flatter is because this ICP is making use of the core value proposition and is not swayed by any other competing product. For this ICP, the one click check out is one of a kind.

For Casual Cory, there is a slightly steeper retention curve and potential reasons for that could be that this ICP has a few more alternatives available. This ICP is loyal but can find greater value in credit cards that allow them to collect more points and is available EVERYWHERE.

While Simpl's merchant base has reached 26000, it has increased recently. Therefore, in the recent past, users could be churned to have grander access to merchants. Something that Casual Cory could have switched for.

Reasons for Churn | Voluntary | Involuntary |

|---|---|---|

Better Rewards on Credit Card Tendency to forget to clear Simpl Bill Did not understand how the product works | Not ordering as much online anymore Increasing fraud in the world Change in preference regarding openness to credit payment options | |

Going back to user insights, the number one reason for users to churn was better rewards on credit cards, followed by forgetting to clear Simpl Bill. This insight came from speaking to churned users.

User 1 : I stopped using Simpl as I use multiple payment options on various platforms. So, I would forget to clear the Simpl bill. I know they send reminders but it just got missed a couple of times.

User 2: I tried Simpl because it looked super convenient, while ordering food. But it doesn't give the best deal a lot of times. Also, it is present on select platforms. Credit cards are just way cooler with respect to lounge access/points and are great when traveling internationally. So, I tend to use that now as a standard payment option.

Negative actions to look out for to identify churned users

- Number of users who are paying the late fee for clearing the bill. If this number is increasing, it means the reminder system is not working, which means the user is unable to experience the core value proposition of one time payment in 15 days without any fee or charge. Therefore, this user is at risk of churn.

- Number of users clearing the Simpl bill via the payment link, and not through the app. If this number is increasing, it implies users are not experiencing the core value proposition of transparency. Without the app, the user is unable to track number and volume of transactions, thereby not experiencing the benefits.

The insights you've shared provide a great foundation to analyze Simpl's user retention trends, user behaviors, and the factors influencing churn. To elevate this analysis, we can connect these findings to broader industry insights, particularly in payment products, consumer behavior, and retention strategies. Here’s how we can integrate your observations with industry trends and further refine the strategy:

Broader Industry Insights:

- The Power of Word-of-Mouth Marketing (Jenny Z ICP)

- Industry Trend: Word of mouth (WOM) continues to be one of the strongest drivers of customer acquisition, particularly in younger generations. According to Nielsen’s 2020 Global Trust in Advertising report, 92% of consumers trust recommendations from friends and family over any other form of advertising.

- Connection to Jenny Z ICP: Jenny Z users, who are advocating for Simpl, are likely in the younger demographic that values convenience, tech innovation, and peer recommendations. Their retention curve is flatter because they are using the core value proposition (one-click checkout) frequently and consistently, which aligns with industry data indicating that younger consumers are highly loyal to brands that meet their immediate needs with simplicity and ease.

- Strategic Insight: Simpl can further capitalize on word-of-mouth and advocacy by building referral programs, engaging Jenny Z users through social media, and empowering them to become brand ambassadors. Simpl could also explore partnerships with influencers in the space to amplify WOM.

- The Loyalty-Reward Challenge (Casual Cory ICP)

- Industry Trend: Credit card companies and digital wallets have increasingly offered more attractive rewards programs, such as cash-back, travel points, and access to exclusive benefits. According to a 2023 study by J.D. Power, the most popular reason consumers choose a specific payment method is the rewards they can accrue.

- Connection to Casual Cory ICP: Casual Cory’s loyalty is being tested by credit cards offering greater rewards and benefits (e.g., travel perks, point accumulation). The increasing competition from credit card companies aligns with the broader trend where consumers are more willing to switch payment methods for better rewards. Furthermore, the fact that Cory is more likely to switch to options that offer value across a broader range of merchants speaks to the rise of universal payment systems (e.g., digital wallets, integrated platforms) that serve as a one-stop solution.

- Strategic Insight: Simpl could explore creating partnerships with more merchants to broaden its appeal or develop unique, compelling reward systems (e.g., simplifying loyalty points or integrating exclusive perks) to differentiate itself from credit card providers. Offering partnerships with travel or lifestyle brands could target users like Cory who are motivated by rewards and travel benefits.

- The Impact of Platform Availability (Casual Cory ICP)

- Industry Trend: Availability on multiple platforms is crucial for retention. Users are increasingly adopting multi-platform usage, and if a service is available only on select platforms, it can create friction in the customer experience. According to PwC’s 2020 Global Consumer Insights Survey, 73% of consumers want brands to provide a seamless, consistent experience across all touchpoints.

- Connection to Casual Cory ICP: Cory’s tendency to prefer widely available payment options underscores the importance of multi-channel access. If Simpl is not integrated on popular e-commerce sites or platforms, this friction can lead to churn.

- Strategic Insight: Expanding the merchant base and increasing platform accessibility would improve retention. Simpl should focus on integrating with major e-commerce platforms, digital wallets, and other online retailers to ensure customers can use it wherever they shop.

- User Forgetfulness & Financial Discipline (Churn Causes)

- Industry Trend: Forgetting to make payments on time is a common pain point in financial products. Companies like credit card providers have focused heavily on user reminders, automated payments, and financial discipline tools. A 2021 report by FICO found that 40% of people use some form of automated payments to avoid missing due dates.

- Connection to Churn (Forgetting to Clear the Bill): User feedback (e.g., User 1) about forgetting to clear the Simpl bill highlights a critical challenge in user experience. This problem is not unique to Simpl, as it’s a common pain point in the payment industry. However, failure to address this can create a gap between users experiencing the core value proposition (paying bills on time without fees) and the reality (forgetting payments and incurring late fees).

- Strategic Insight: Improving reminder systems (e.g., in-app, email, SMS reminders) is critical. Additionally, Simpl could offer more seamless ways for users to auto-clear their bills or enable a feature that allows users to “pause” payments temporarily to avoid accruing late fees. A rewards or incentive system for on-time payments could also drive positive financial behaviors.

- The Risk of Fraud (Increasing Fraud in the World)

- Industry Trend: Payment fraud is an ever-growing concern. According to a 2022 report by the European Central Bank, payment fraud has been on the rise, with digital transactions being particularly vulnerable to fraud attempts.

- Connection to Churn (Fraud Concerns): As fraud becomes more prevalent, users are becoming more cautious about sharing payment details. Users may be hesitant to use Simpl if they perceive any risk in terms of security or fraud prevention, contributing to churn.

- Strategic Insight: Simpl should focus on enhancing security measures, such as two-factor authentication (2FA), end-to-end encryption, and fraud monitoring systems. Communicating these security features clearly to users will help build trust and reduce concerns about fraud.

Strategic Recommendations:

- Strengthen Advocacy with Jenny Z (Word of Mouth):

- Foster user advocacy through referral programs, influencer collaborations, and creating exclusive experiences for high-value users. Simpl should leverage the WOM strength of Jenny Z to organically grow its user base.

- Develop gamified referral incentives where users are rewarded for sharing Simpl with others or leaving positive reviews.

- Enhance Rewards & Value Proposition for Casual Cory:

- Consider integrating more robust reward systems that appeal to Cory’s love for credit cards and travel rewards. Partnering with airlines, hotels, or online retailers could provide compelling reasons to use Simpl over other payment options.

- Expand the merchant base to make Simpl more universally accepted across major platforms, ensuring Cory doesn’t feel the need to switch.

- Address Payment Reminders and Automation:

- Improve the reminder system and enable features like auto-payment or "payment pause" for users who might forget to clear their Simpl bill. This would reduce friction and ensure users continue to enjoy Simpl's core value proposition.

- Introduce incentives for on-time payments or a loyalty program that rewards financial discipline, which could further increase user retention.

- Increase Focus on Security and Fraud Prevention:

- Given the rise in fraud, Simpl should ensure users feel confident in the security of their transactions by highlighting security features. Regular updates on fraud prevention and secure payment methods can help increase trust and reduce churn.

By connecting Simpl’s retention and churn insights with broader industry trends, strategies can be fine-tuned to meet user needs more effectively, enhance retention, and reduce churn.

Brand focused courses

Great brands aren't built on clicks. They're built on trust. Craft narratives that resonate, campaigns that stand out, and brands that last.

All courses

Master every lever of growth — from acquisition to retention, data to events. Pick a course, go deep, and apply it to your business right away.

Explore courses by GrowthX

Built by Leaders From Amazon, CRED, Zepto, Hindustan Unilever, Flipkart, paytm & more

Course

Advanced Growth Strategy

Core principles to distribution, user onboarding, retention & monetisation.

58 modules

21 hours

Course

Go to Market

Learn to implement lean, balanced & all out GTM strategies while getting stakeholder buy-in.

17 modules

1 hour

Course

Brand Led Growth

Design your brand wedge & implement it across every customer touchpoint.

15 modules

2 hours

Course

Event Led Growth

Design an end to end strategy to create events that drive revenue growth.

48 modules

1 hour

Course

Growth Model Design

Learn how to break down your North Star metric into actionable input levers and prioritise them.

9 modules

1 hour

Course

Building Growth Teams

Learn how to design your team blueprint, attract, hire & retain great talent

24 modules

1 hour

Course

Data Led Growth

Learn the science of RCA & experimentation design to drive real revenue impact.

12 modules

2 hours

Course

Email marketing

Learn how to set up email as a channel and build the 0 → 1 strategy for email marketing

12 modules

1 hour

Course

Partnership Led Growth

Design product integrations & channel partnerships to drive revenue impact.

27 modules

1 hour

Course

Tech for Growth

Learn to ship better products with engineering & take informed trade-offs.

14 modules

2 hours

Crack a new job or a promotion with ELEVATE

Designed for mid-senior & leadership roles across growth, product, marketing, strategy & business

Learning Resources

Browse 500+ case studies, articles & resources the learning resources that you won't find on the internet.

Patience—you’re about to be impressed.